# Jimmy's Architecture

Jimmy represents a new class of autonomous hedge fund managers designed to handle spot, perpetual, and options markets in real time. Building upon cutting-edge multimodal architecture and reflective learning frameworks. Jimmy employs Market Intelligence, Memory, Reflection, and Tool-Augmented Decision-Making to deliver robust performance across diverse market conditions.

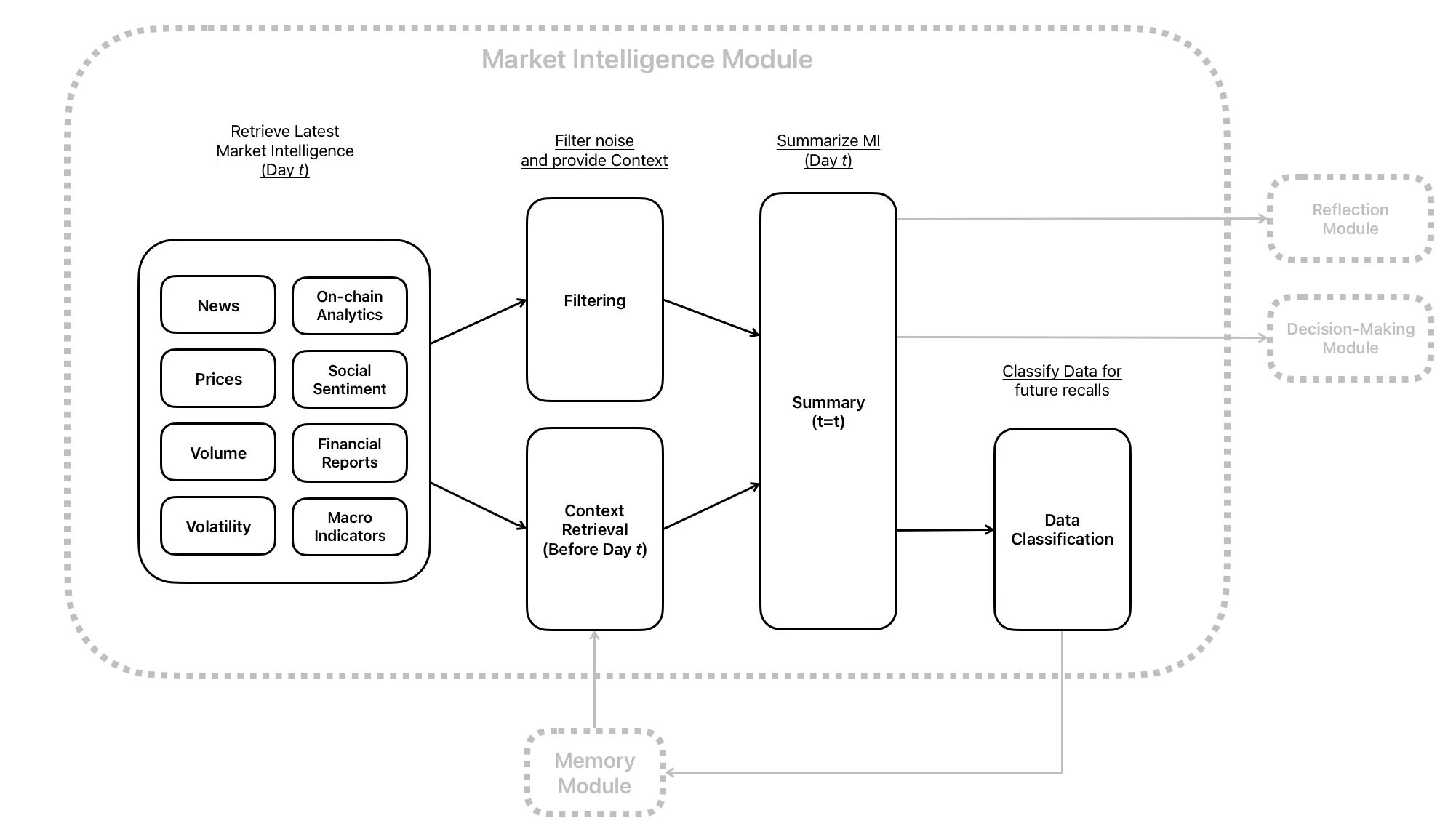

Jimmy's Architecture

***

### Market Intelligence Module

The Market Intelligence Module enables real-time situational awareness by consolidating diverse data sources. This module results crucial for high-level financial decision-making, ingesting:

* **High-frequency on-chain analytics** (e.g., transaction volumes, liquidity outflows).

* **Exchange-level orderbook data** (e.g., best bid/ask spreads, depth of market).

* **Macroeconomic indicators** (e.g., interest rates, inflation data).

* **Text-based intelligence** (e.g., social sentiment, financial news, regulatory updates).

* **Visual signals** (e.g., annotated K-line charts, candlestick patterns, or volatility histograms).

#### Architecture and Process

1. **Data Retrieval and Filtering**\

Jimmy retrieves diverse market intelligence from blockchain analysis, exchanges, financial reports, etc. Custom relevancy filters minimize noise.

2. **Contextual Summarization**\

Summaries combine immediate market sentiment, historical precedents, and technical overlays, allowing subsequent modules to interpret a coherent “snapshot” of market conditions.

3. **Diversified Retrieval**\

Jimmy classifies data by retrieval type (e.g., short-term volatility vs. medium-term sentiment). This ensures more precise archival and recall of relevant past events.

***

### Memory Module

The Memory Module provides Jimmy with data-driven adaptation capabilities thanks to a **contextually aware** retrieval system that helps Jimmy preserving context and refining learned behaviour over extended time periods. Jimmy’s memory accomplishes this by:

* **Storing** all summaries, reflections, and outcomes.

* **Vectorizing** textual data and relevant numeric features for semantic retrieval.

* **Enabling** high-speed lookup of historically similar market conditions (e.g., correlated volatility patterns, analogous news events).

#### Architecture and Process

1. **Long-Term and Short-Term Memory** \

The Short-Term memory maintains immediate (intra-day or daily) data useful for high-frequency trades. The Long-term memory archives monthly or quarterly trends and reflection outputs, enabling detection of cyclical macro patterns.

2. **Embedded Vector Index**\

Employs dense embeddings to facilitate similarity searches among historical states.

3. **Adaptive Recall**\

Dynamically retrieves either short-term or long-term memories based on the retrieval types flagged by the Market Intelligence module.

***

### Reflection Modules

Inspired by human cognitive learning Jimmy integrates two reflection layers, low-level (low timeframe) and high-level (high timeframe) reflection, ensuring robust performance in both volatile micro-trends and broader macro cycles.

#### Architecture and Process

1. **Low-Level Reflection**\

Low-level reflection deals with immediate market fluctuations, such as minute-to-minute or hourly changes. By examining how granular data—like technical signals and breaking news—translates into real-time price shifts, this reflection process reveals key cause-and-effect insights. These insights are then stored in the Memory Module, allowing the system to quickly adapt to short-term volatility and refine its tactical responses.

2. **High-Level Reflection**\

High-level reflection addresses longer time horizons and assesses the cumulative performance of the portfolio over multiple days, weeks, or months. It examines how well various strategies work together—whether they reinforce or conflict with one another—and evaluates the overall consistency and effectiveness of the trading approach. Based on these findings, it produces a strategic review that highlights systemic strengths or weaknesses, which in turn guides future decision-making within the platform.

***

### Tool-Augmented Decision-Making Module

Jimmy’s Decision-Making Module integrates specialized external tools and user-defined preferences to execute trades. This component interprets outputs from the Market Intelligence, and Reflection modules to form data-enriched decisions.

#### Architecture and Process

1. **Integrated Strategy Selection**\

Jimmy dynamically filters from a broad repository of trading strategies—ranging from delta-neutral to trend-following and long/short options—to identify the most suitable approach under current conditions. \

As it processes real-time market signals, Jimmy aligns each trade with the strategy most likely to succeed.

2. **Professional Tools**\

In addition to its own analysis, Jimmy leverages established financial heuristics like MACD cross or RSI divergence, as well as sophisticated risk models such as VaR constraints. It also deploys specialized execution optimizers to manage trades efficiently. \

Where needed, the system can integrate external “expert-coded” modules to address unique scenarios—for example, a sudden change in interest rates or a major token unlock event.

3. **User Constraints and Execution**\

Throughout its decision-making, Jimmy respects user-defined parameters, such as maximum drawdown, VaR thresholds, or sector-specific restrictions. \

By integrating with AskJimmy’s multi-chain framework, Jimmy can route trades strategically to minimize slippage and ensure best execution across multiple venues.

4. **Process Flow**\

Jimmy begins by consolidating the latest summaries, reflection outputs, and any relevant data retrieved from its memory. It then conducts an internal Chain-of-Thought analysis, carefully weighing potential options and their implications. Once the reasoning phase is complete, Jimmy issues a clear action plan accompanied by the rationale behind the chosen action.

***

### References

1. Zhang, W., Zhao, L., Xia, H., et al. (2024). *A Multimodal Foundation Agent for Financial Trading: Tool-Augmented, Diversified, and Generalist*. KDD ’24.

2. Chen, T., Heaton, J.B., Polson, N., & Witte, J. (2023). *Deep Learning in Finance*. SSRN.

3. Brown, T., Mann, B., Ryder, N., et al. (2020). *Language Models are Few-Shot Learners*. NeurIPS.

4. Li, W., Yin, C., & Chen, L. (2022). *Survey on AI-driven Financial Markets*. IEEE Transactions on Neural Networks.

5. Liu, S., Wang, X., Yu, K. (2023). *Integrating Vector Databases for LLM Retrieval*. arXiv.